Car insurance claims don’t always go smoothly. Sometimes the numbers simply don’t add up. The insurer estimates one repair cost while your mechanic insists the real number is much higher. Suddenly the claim stalls, and you’re left wondering who decides the true value.

This is where an appraisal clause auto insurance provision can completely change the outcome.

Most drivers never notice this clause until a dispute appears. Yet it sits quietly inside many auto insurance policies, ready to resolve valuation disagreements when negotiations fail. It isn’t a courtroom fight. It’s not arbitration either. Instead, it’s a structured process that brings in independent experts to determine a fair value for vehicle damage or repairs.

I’ve seen many policyholders accept lower claim payouts simply because they didn’t realize this option existed. The appraisal clause provides leverage. It introduces neutral voices. And it often resolves disputes faster than traditional legal routes.

Let’s unpack how it works and how you can use it if your claim hits a wall.

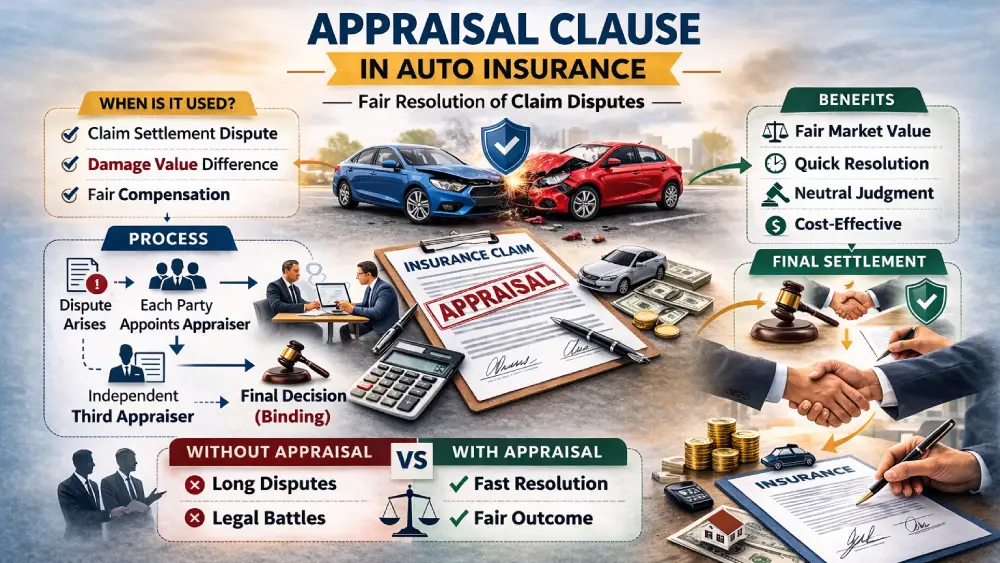

What Is an Appraisal Clause in Auto Insurance?

An appraisal clause auto insurance provision allows disputes over the value of a claim to be resolved through independent appraisers rather than relying solely on the insurer’s estimate.

Think of it as a professional tie-breaker.

When both parties agree that damage is covered but disagree about the price tag, the clause allows each side to appoint an appraiser. These appraisers analyze repair estimates, inspect the vehicle, and review market values. If they cannot agree, a neutral umpire helps finalize the decision.

The goal is simple: determine the correct value of the loss.

Common scenarios where appraisal clauses appear include:

- Repair estimate disagreements

- Total loss value disputes

- Diminished value claims

- Specialty or classic vehicle valuations

One key detail matters here. The clause resolves value disputes, not coverage disputes. If an insurer says the damage isn’t covered at all, the clause typically does not apply.

How the Auto Insurance Appraisal Process Works

The appraisal clause auto insurance process follows a clear and structured series of steps. While policies vary slightly, the core framework remains consistent.

Step 1: A Disagreement Occurs

Everything begins with a valuation dispute.

You file a claim. The adjuster inspects the vehicle and produces a repair estimate. But the numbers don’t match what your mechanic or body shop sees.

For example:

| Estimate Source | Repair Cost |

| Insurance Adjuster | $4,800 |

| Repair Shop | $7,100 |

That difference can halt progress quickly.

Step 2: The Appraisal Clause Is Invoked

At this stage, either party may trigger the appraisal clause.

Most policyholders begin by sending a written request referencing the clause in their policy. Once invoked, both sides begin selecting independent appraisers to evaluate the loss.

Documentation becomes crucial here. Photos, estimates, vehicle condition reports, and repair notes all strengthen the review.

Step 3: Each Side Selects an Appraiser

Both parties appoint their own expert:

- The policyholder’s independent appraiser

- The insurance company’s appraiser

These professionals inspect the vehicle, review estimates, and analyze market values. Their job is not to argue—it’s to determine a fair number based on evidence.

However, experience matters greatly here. A well-qualified appraiser can provide stronger documentation and more accurate valuations.

Step 4: An Umpire Is Selected

If the two appraisers cannot agree on a value, they appoint a neutral third party called the umpire.

The umpire evaluates the evidence presented by both appraisers and makes the final determination if needed.

Two out of three votes determine the final amount

When an Appraisal Clause Is Used

Not every claim dispute qualifies for appraisal. The appraisal clause auto insurance process is designed specifically for valuation disagreements.

Here are common situations where it’s used.

Total Loss Value Disputes

After a serious accident, an insurer may declare a vehicle a total loss and offer a settlement based on market value.

However, drivers often discover that comparable vehicles used in the calculation differ significantly in mileage, trim, or condition.

Appraisal can correct those discrepancies.

Repair Cost Disagreements

Repair shops and insurance adjusters often use different pricing models.

Insurance software may estimate lower labor costs or fewer parts replacements than local shops recommend.

Appraisal allows independent professionals to evaluate the damage objectively.

Diminished Value Claims

Even after repairs, a vehicle may lose resale value due to its accident history.

Determining the amount of lost value can be highly subjective, making appraisal a valuable tool.

Specialty Vehicle Valuation

Classic cars, modified vehicles, and luxury models often require specialized valuation expertise.

Standard pricing databases may not accurately reflect their true value.

Independent appraisers bring deeper automotive knowledge to these cases.

Benefits of the Appraisal Clause

The appraisal clause auto insurance provision exists to solve disputes efficiently. When used correctly, it offers several advantages.

Faster Resolution

Court cases can take months or even years. Appraisal disputes often resolve within weeks.

Lower Costs

Legal battles involve attorney fees, court costs, and expert witnesses. Appraisal usually requires only the cost of hiring an appraiser.

Balanced Decision Making

Instead of relying solely on an insurance adjuster, the process includes multiple independent professionals reviewing the claim.

Increased Negotiation Leverage

Once the appraisal clause is invoked, insurers often become more willing to negotiate fairly.

Potential Drawbacks of the Appraisal Process

While powerful, the appraisal process does come with limitations.

Appraiser Fees

Policyholders typically pay for their own appraiser. Fees can range from $300 to $1,500 depending on the complexity of the claim.

Limited Scope

The clause only determines claim value. Coverage disputes must be resolved through other legal avenues.

Appraiser Quality Varies

Choosing the right professional matters. Inexperienced appraisers may weaken a claim.

How to Trigger the Appraisal Clause

Invoking the appraisal clause auto insurance process is straightforward if you follow these steps.

1. Review Your Policy

Locate the appraisal clause section within your auto insurance policy.

2. Submit a Written Request

Send a written notice to your insurer referencing the appraisal clause and your claim number.

3. Hire an Independent Appraiser

Choose someone experienced in auto insurance claim disputes.

4. Prepare Supporting Documentation

Helpful documents include:

- Repair estimates

- Vehicle photos

- Maintenance records

- Comparable vehicle listing

- Market valuation reports

The stronger your documentation, the smoother the process becomes.

Tips for Choosing a Good Appraiser

Selecting the right expert can significantly influence the outcome.

Look for professionals who have:

- Experience with insurance appraisal disputes

- Certification or automotive valuation training

- Knowledge of local repair markets

- Strong documentation and reporting skills

Many independent auto damage consultants specialize in appraisal clause disputes.

Before hiring, ask about their previous cases and reporting methods.

Appraisal vs Arbitration vs Lawsuits

These dispute resolution methods often get confused.

| Method | Purpose | Speed | Cost |

| Appraisal | Determine claim value | Fast | Moderate |

| Arbitration | Resolve broader disputes | Medium | Higher |

| Lawsuit | Legal disputes and coverage issues | Slow | Expensive |

For simple valuation disagreements, appraisal is often the most efficient option.

Example Appraisal Clause Case

Consider this scenario.

A driver files a claim after a rear-end collision. The insurance adjuster estimates repairs at $5,200. The body shop estimates $8,900 due to structural damage.

Negotiations stall.

The policyholder invokes the appraisal clause auto insurance provision.

Each side hires an appraiser. After inspection:

- Insurance appraiser: $6,100

- Policyholder appraiser: $8,200

An umpire reviews the reports.

Final decision: $7,600.

The insurer pays the updated amount, and repairs proceed.

Without appraisal, that dispute might have dragged on for months.

Final Thoughts

Insurance claims can become frustrating when valuations don’t match expectations. But policyholders are not powerless.

Understanding the appraisal clause auto insurance process provides a practical path forward when negotiations stall. It introduces independent experts, encourages fair valuations, and resolves disputes far more efficiently than litigation.

If you ever feel that your claim estimate is significantly undervalued, review your policy carefully. That small clause buried in the fine print could be the tool that restores balance to the process.

And sometimes, that’s exactly what a complicated claim needs.

Frequently Asked Questions

It is a policy provision that allows claim value disputes to be resolved by independent appraisers instead of relying solely on the insurer’s estimate.

You should consider using it when you and the insurer agree the damage is covered but disagree on the cost of repairs or the vehicle’s value.

Both the policyholder and the insurance company each select their own independent appraiser to evaluate the claim.

They select a neutral umpire who reviews the evidence and helps determine the final claim amount.

Typically, each party pays for their own appraiser, and the cost of the umpire is shared between both sides.

Many appraisal disputes are resolved within a few weeks, though complex claims may take longer depending on inspections and documentation.

No. The appraisal process only decides the value of the claim, not whether the insurance policy covers the damage.

Collect repair estimates, photos of the damage, vehicle records, and any comparable market value information.

In most policies, the decision becomes binding for the claim amount once two of the three participants agree.

Many policies include one, but it’s important to review your policy wording to confirm if it applies.